|

2020 has been a crazy year, but we are only at the mid-point. This video is a recap of global macro data. Here are the key takeaways - Data around the world looks similar - Worst impact of the pandemic is behind us - Global fiscal and monetary stimulus is helping - Expect economies to improve over the next 12 months ---

This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.

2 Comments

Leonardo Da Vinci dissected cadavers to understand the intricacies of the human body. Dissections improved his ability to paint and sculpt. Here is a link to Leonardo Da Vinci: Lessons from the original polymath. Medical students dissect cadavers to study anatomy. Business discussions on TV or by your local water cooler, however, are dominated by growth rates or Price to Earnings ratios. These metrics are short cuts to business analysis. However, this analysis is superficial unless it includes the dissection of the most important metric – unit economics.

What is the meaning of unit economics? Simply put, understanding unit economics is focusing on the core business activity at a grass-roots level. Building on this core metric determines the true long-run profitability of a business. Let me show you how to break down the unit economics for any business. The How-To Guide. For any unit-based business, whether a doctor’s clinic, a retail or restaurant chain, the goal is to understand the profitability of each unit. We can accomplish this by disaggregating this process into several steps: 1) The investment required to build or lease the unit/office. 2) The sustainable revenues this unit can generate when fully functional. 3) The total cash flow that this unit can generate. 4) Armed with this knowledge, we can calculate the payback of each unit. A software or internet business has upfront fixed costs but low marginal costs. For example, a business must build its technology infrastructure before it can acquire customers. Once the application is ready, it can theoretically serve as low as a one, to as high as an infinite number of customers. Therefore, it is important to understand the return on investment in acquiring new customers. We can accomplish this by disaggregating this process into several steps: 1) The continuous investment in sales/marketing and R&D to acquire customers. 2) The revenues generated from an annual subscription 3) The cash flow this business would keep after paying for costs. 4) Using this information, we can calculate the payback on customer acquisition. Rapid sales growth, by itself, is not a marker of a good business. Technology businesses sport high growth rates, but most lack customer loyalty, which makes the growth rates misleading. Acquiring or building new units, with bad unit economics, dilutes the total value of the business – despite the revenue growth. Raising capital is frowned upon by investors because it dilutes existing shareholders, but if pursued to accelerate business with strong unit economics, it increases the total value of the business. Therefore, just looking at business growth or Price to Earnings ratio is a superficial analysis. In short, when it comes to business comprehension, one must be willing to get their hands dirty. When in doubt, dissect. If it worked for Leonardo, it will work for you and me also. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. A combination of unprecedented fiscal and monetary support is healing businesses and consumers at a faster rate. Despite widespread investor pessimism, all asset classes are validating the current market rally - leading to Breakaway Momentum - a rare signal suggesting strong 12-month future returns. In this video, I present the evidence that we are in a new bull market, and buying market corrections is the right strategy. ---

This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. Ownership of a toll road like business is a lucrative opportunity. The upfront investment is large; therefore, competitors think long and hard about building another one. Once a toll road is built, the upkeep is small. The number of cars passing through increases every year, while the cost to let an incremental vehicle through is minuscule. Congestion can discourage additional cars. The owner can raise prices gradually over time. Therefore, toll roads provide a predictable, stable, cash flow stream for years and years to come.

President Eisenhower had an appreciation for the German Autobahn system and wanted to build a transportation network for the U.S. This desire gave rise to the Federal Highway Act of 1956 which led to the large-scale construction of the public infrastructure that we use to this day. Majority of this infrastructure is owned by Governments. While there are a growing number of public-private partnerships that large institutional investors could participate in, most infrastructure investments are out of reach for the individual investor. Until now. The toll roads of the 21st century that are under construction today are digital. The fixed costs are still high, and the marginal costs are even lower. The thru-put capacity is virtually infinite. The good ones are built to last and ownership in these will be lucrative. Here is the best part – anyone can acquire pieces of these publicly traded toll roads through careful research. Cloud infrastructure is a great example. As time marches on, more data and computing power move into the cloud. It is an inevitable trend. Due to the mega-scale economics of cloud infrastructure companies, the price plus convenience value proposition is attractive. This offering has turned a deliberation into an easy decision for small to large businesses to say goodbye to their own servers. Only 10-15% of total data has made its way into the cloud, but the transition is accelerating. A growing number of applications are being built on top of cloud infrastructure to solve business problems. The new pricing architecture is consumption-based, which makes it much easier to embrace. Communication platforms are another type of digital toll road. We know that digital communication is here to stay. Businesses need to evolve to this new norm to acquire new customers, interact with existing consumers, or risk their own demise. More and more companies are building their own applications on top of these platforms tailored to their business needs. The larger the frequency of traffic, the more valuable it makes the underlying toll-road. There are many more examples. Digital transformation is a top business priority. The digital traffic will rise exponentially over the next decade, which makes these 21st Century Toll Roads incrementally more lucrative than the ones of the past. The best part is – you and I can be owners in these toll roads. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  The digital attack on cold, hard cash and checks has gained momentum for the past decade. As digital payment systems have evolved, so have their ease of use. This ease has made a visit to an ATM or writing a check - not only an arduous task – but an unnecessary one. The growth in peer-to-peer systems, the proliferation of frictionless payments (e.g. Uber) has made this a smooth transition. But in a Covid-19 world, the use of cash has graduated from inconvenient to hazardous. Cash is a virus transfer mechanism.

I fully expect a growing number of retail outlets to offer digital payment options, and an even greater number of consumers to demand these options. Why exchange a credit card when you can make a payment on your phone and eliminate all risk? It takes a substantial upfront investment to build a true payment network infrastructure to process the first transaction. Once built, the incremental transaction has low marginal costs. Simply put, Payment networks are a high fixed cost and low marginal cost models. They are also scalable, which makes incremental profitability significant and sustainable. Our societal behavioral change only feeds the network effects of Payment business models. These network effects are extraordinarily strong. The increase in the number of consumers (demand) brings more merchants onto the platform (supply) which makes the network better and easier to use, with more perks. A higher-quality network then attracts even more consumers. The snowball keeps rolling downhill at a faster and faster pace. China has led the digital payment revolution, a place where cash belongs in museums. China entirely skipped the credit card phase. The proliferation of mobile devices and the rise of dominant digital payment models of AliPay (Alibaba) and TenPay (Tencent) has defeated cash. The longer it takes for a treatment to be introduced, the deeper our habits are ingrained. When we return to a virus-free world, we as consumers will wholeheartedly embrace our favorite experiences; those being travel, concerts, and sporting events. A visit to an ATM will not be on that list. We have built all the essential payment infrastructure, and we are accelerating our transition to a cashless society. This will be a boon for Payment businesses and profitability will explode along with it. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. Malcolm Gladwell’s Tipping Point is one of my favorite books. The book talks about how little things can make a big difference, but what happens when big things tip the scales in your favor. Let us explore why changing behaviors in a Post Covid-19 world can tip Ecommerce towards sustained profitability.

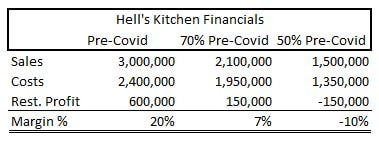

An internet retail business has two significant but distinct investments: 1) a fixed cost investment in logistics and 2) a variable cost investment to acquire customers. While most e-commerce businesses have grown sales at a blistering pace over the past decade, the unit economics are attractive for only a small subset. Simply put, logistics are expensive to build, and customers are expensive to acquire. But the latter is also fickle. In other words, repeat transactions are hard to come by, and companies must keep spending on marketing and discounts to bring customers back. Therefore, despite the rapid sales growth and share gain from traditional retail, profits are hard to come by. The other obvious reason is the dominant position of Amazon. It comes as a shock to no one that most shopping intent starts on Amazon. However, the positive demand shock from social distancing is even too much for Amazon to handle. The company is only delivering essential items as even the Amazon machine cannot handle this influx of orders. Suddenly, customers are forced to look elsewhere. Physical retail was already weak and now could be permanently impaired even after reopening. The silver lining in a sea of high unemployment is that the majority of the population is still employed. While this employed group might look to cut down on their spending, they have a few places to spend. Without Amazon or traditional retail in the way, this influx of new business is served on a platter to E-commerce companies. This acceleration is moving internet retail towards a tipping point. A profitability tipping point. The flood of order volume is doing wonders to leverage the high fixed costs. But to put the icing on the cake, customers are flocking to these businesses on their own. No advertising needed. The longer the threat of COVID lasts in our society, the more repeatable and entrenched will customer actions and preferences become. How could this not be a significant boon to E-commerce businesses? This surplus cash flow will be reinvested in faster logistics and to lower the cost of operations. The compounding effects will strengthen these companies in the long run. Business moats will be entrenched. We may be in the very first inning of this acceleration. Most businesses are moving in reverse in a COVID world, but E-commerce is tipping towards sustained profitability. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  After spending several weeks sheltered at home, we are all looking forward to having a great meal with friends at our favorite restaurants. Unfortunately, for most restaurants, and the "Mom & Pop" industry in general, the journey through this valley is going to be arduous. It will be Hell’s Kitchen. Here is why. The restaurant industry is economically sensitive and runs on thin margins to begin with. The need of its patrons to now socially distance themselves, in addition to massive unemployment and less patrons overall, is a one-two punch. During high unemployment such as the present time, patrons generally forgo weekday meals and high margin items (appetizers, drinks, and desserts) to find a balance between eating out and saving. During weekend peak hours, restaurants will operate with fewer tables, so patrons are socially distanced. However, a 30% drop in revenues is enough to wipe out the profitability of the business. Anything below that and most restaurants must close. Please see the illustration below to understand these numbers. This restaurant - Hell’s Kitchen - has sales of $3 million per year and profitability of $600k. Cost of food, labor, and other operating expenses is 80% of revenues. There are additional overhead costs, buts let’s forget those for now. In a normal world, Hell’s Kitchen is a profitable restaurant and the envy of most "mom & pop" restaurateurs. But in a Corona virus world, most of the profitability is wiped away at 30% decrease in revenues. And believe me, it will take a herculean effort to regain those sales. If the best are likely to struggle, what are the chances of the average restaurant business to survive in this new world?  The outlook is grim and requires extreme creativity on the part of the restaurateur. They will have to find ways of filling tables during off-peak hours, work extra hard to grow the takeout and delivery business, and find ways to reduce costs. This means working with the landlord to reduce rents, and other service providers to find payment relief. We as consumers also play a part in this recovery. Those who have the means must make a concerted effort to order from their favorite local restaurants. Ultimately, small businesses are the cornerstone of every community and without them, no community will be the same. The restaurant business is fighting an enemy like never before, and we can all play a part in helping them stay in this fight.

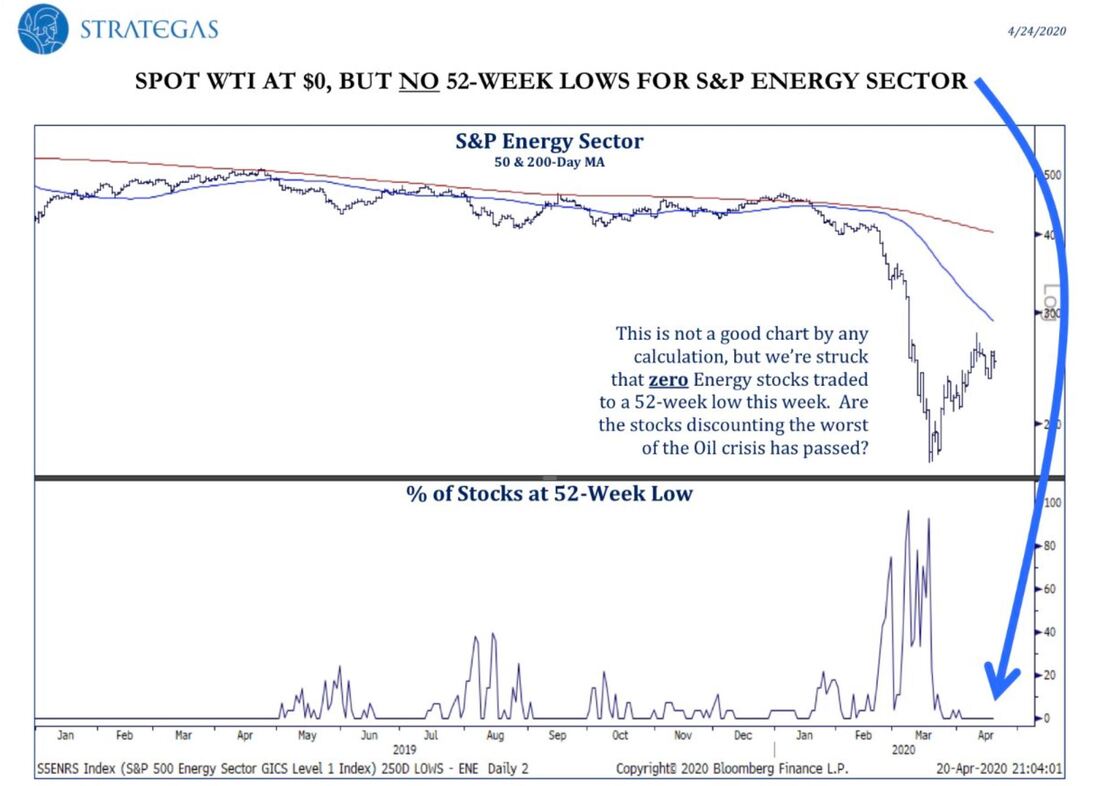

--- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. What a week it was! Oil prices plunged, but they did not stop at zero. At one point during the week, the price of the expiring current month Crude oil contract was negative $40 dollars. Did anyone think this was possible? Theoretically, this price quotation would suggest that a producer of Crude oil was paying the buyer $40 dollars to take a barrel of crude off his or her hands. Although this transaction did not happen in the real world and negative prices were mostly a technical issue, traders were caught on the wrong side of an illiquid market and option volatility accelerated the decline.

Here is a fundamental difference in commodities vs. stocks. The physical supply vs. demand plays a major part in determining the price of a commodity, and when a market is oversupplied, prices move lower to dis-incentivize production. When consumers are stuck at home and storage is filling up in the U.S., lower oil prices are forcing producers to shut off the oil spigots. Oil prices will not rebound until economies get back on their feet and the oversupply is reduced. Stock prices in the short term also depend on the supply vs. demand of buyers and sellers, but the value of businesses over the long term are based on the cash flows they produce well into the future. And here is where this week gets interesting. While crude oil was plunging to depths unknown to investor kind, stocks of oil producers did not follow commodity prices. Take a look at this interesting analysis (LINK). Most energy stocks were positive and did better than the overall market for the week. This is simply because most future month Crude prices did not plunge the same way spot prices did, and stocks anticipated that bad news was coming. A good rule of thumb is that by the time a news event reaches PAGE 1 status, it is very well discounted in (anticipated by) stock prices. In layman terms, energy stocks are pricing in a bad future. Reality can always get worse. However, stocks are a long-duration asset. While short term events create volatility that takes a toll on the human psyche, it does not impact the long-run valuation of the business. This week is the beginning of a bottoming process for energy. If you are looking for background, read The Bottom of The Barrel. Undoubtedly, this will be a long process. Many producers will have to restructure their businesses depending on their debt loads. Lots of service providers will not make it to the other side. But downcycles are opportunities for the best companies – with low cost resources and excellent balance sheets – to capitalize on the mismanagement of others. This economic Darwinism is much needed to repair the oversupply and put the entire energy patch on good footing again. -- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  After six weeks of the unthinkable, economic rubble is high. We have lost 22 million jobs – of a base of 155 million employed Americans – bringing the unemployment rate to almost 15%. After accounting for the number of Gig economy jobs and extra income that is lost – the total damage is significantly higher. The downstream impact – the industries supporting the businesses that are in the eye of the storm – is hard to calculate. But undoubtedly there is additional damage. Many businesses are permanently impaired. These are some of the reasons for markets to be down and stay down.

But markets around the world are rebounding. How is that possible? Here are the key reasons for the markets’ optimism. The Federal Reserve has a ‘do whatever it takes’ stance and has attacked lending weakness with lightning speed. Markets crave liquidity. The Fed cannot generate demand, but this is where Congress steps in. 2020 is an election year, and for the first time in history, both sides are on the same page and willing to bail out everyone. The $350 Billion Paycheck Protection Program is already out of money – and undoubtedly more is on the way. Unemployment payments are larger than most low-end salaries and might continue longer than the usual 4 months. Stimulus checks are already hitting bank accounts. There is enough short-term relief to hold the usual negative feedback loop at bay. But the cause for real optimism stems from research labs. For the first time in history, the brightest minds and companies around the world are focused on solving one problem – COVID 19. Betting against human ingenuity has always been a losing proposition. Markets’ are banking on a solution - either a treatment or a vaccine - to arrive much earlier than the usual timeframe. That would be a true game-changer on the way back to the old normal. Over the years, I have learned the hard way that the market is not the economy. In times of chaos, even I need a reminder. Here is a link to 10 Reasons Why the Stock Market Is not the Economy if you need a refresher. The reopening is akin to walking a difficult tight rope, which will bring a set of challenges as well as opportunities. As investors, we need to stay open to this new world - instead of being anchored into a positive or negative position. Markets are an iceberg, and there is considerably more information underneath the surface than at face value. Understanding the direction of interest rates has been critical and we are closing in on another inflection point. The next few weeks hold the key in determining if this is a fleeting rebound or a sustainable one. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. |