What is a ‘Picks and Shovels’ business?

A strategic business that becomes the key cog in bringing a product or service to market and extracts the most value out of the product chain. Here is an alternative, and a simpler explanation straight for Wikipedia: A pick-and-shovel play is an investment strategy that invests in the underlying technology needed to produce a good or service instead of in the final output. It is a way to invest in an industry without having to endure the risks of the market for the final product. The investment strategy is named after the tools needed to take part in the California Gold Rush. The strategy is named after the tools used to mine for gold during the California Gold Rush of the 1840s and 1850s. Prospectors needed to buy a pick and a shovel to be able to mine for gold. While there was no guarantee that a prospector would find gold, the companies that sold picks and shovels were earning revenue and thus were good investments. The Microsoft operating system or the Intel chip are great examples. While the personal computer industry revolutionized the way we worked, PC companies spent most of their time fighting for survival. It was an undifferentiated industry. Even Apple, one of the most innovative companies today, had to pivot its strategy, to avoid bankruptcy. On the other hand, the Microsoft operating system and the Intel chip were the picks and shovels. It did not matter if Dell, Compaq, IBM, or Gateway won or lost the market share battle. As long as consumers bought more PCs, Microsoft and Intel won. Every single time. Here is another example. While air travel provides tremendous benefits to passengers, airline businesses have never captured this value for their investors. Why? Every airline virtually offers the same experience. The cheapest ticket usually wins. To make matters worse, unpredictability with operating conditions (weather), volatile input costs (oil), massive fixed costs, and large investments to buy new planes to improve service standards leave the cash coffers always on empty. However, Aftermarket Parts businesses that support aerospace and defense have enviable track records. They provide cheap spare parts that are critical to fleet repair and maintenance. Airline companies want cheaper parts alternatives, to improve airline profitability. Once a ‘part’ gets approved, it's very sticky. More planes and more travel - lead to more wear and tear - and a greater need for parts. Within the entire value chain, these businesses generate the highest returns on capital. Aftermarket product businesses are the picks and shovels in aviation. This brings us to the newest iteration of Picks and Shovels - The commerce enablers. Covid was a massive catalyst for E-commerce, and I wrote about it early in the pandemic (LINK). Every business was forced to invest in an online presence. Lots of new E-commerce businesses were formed out of necessity last year. To add fuel to the fire - during the time of overwhelming demand - Amazon made a strategic decision to restrict sales to essential consumer goods. Merchants that relied on Amazon, as their sole sales channel, had to rethink strategy and establish other channels to sell. As a result, E-commerce penetration grew more in one year than in the previous half-decade. When most physical retail was closed and we (consumers) were forced to search for buying alternatives, getting customers to buy (customer acquisition) was easy and low (no) cost. Those were the good old days. However, as the world reopens, and we get back to some of our old habits, these E-commerce companies face a different world. Instead of customers coming to them, they must seek them out. Competition has intensified. The only way to grow is to spend generously on digital advertising to acquire new customers. In this world, the picks and shovel companies are the digital enablers. Social media companies - that already have our attention - will attract a disproportionate share of advertising dollars. If history is a guide, a majority of the newly formed E-commerce businesses will struggle. E-commerce requires massive scale in logistics and customer acquisition. The climb to the top of the ‘scale’ mountain is arduous. However, the best advertising businesses will generate strong returns over the foreseeable future. They are the key cog in the wheel. Digital advertising is the pick and shovel play on E-commerce. In Part II, I discuss how Social media companies make money. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.

1 Comment

Over the past decade, Bitcoin has ascended into mainstream investment discussions based on 1) increase in value and 2) the rabid nature of its ownership base. Rather than a programmable network, or a transacting medium, Bitcoin has evolved simply into an investment medium – an alternative commodity of sorts. The 45% drop in value over the past month has ignited the same-old debate on the value and utility of Bitcoin. Bitcoin, along with other Cryptocurrencies, are evolving platforms. Therefore, it is critical to keep an open mind to new information and developments, instead of getting locked into a dogmatic belief that is for, or against. Here is the framework for owning Bitcoin the way I see it today.

Pros of Owning Bitcoin

Cons of Owning Bitcoin

When an asset lacks underlying cash flow, price depends on the emotion of the market. Momentum then becomes the strongest emotion. High prices attract buyers and low prices bring on more sellers. If you look at the large swings in bitcoin over the past decade, momentum is the easiest explanation. It is the ultimate confidence game. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. A faster deployment of vaccines has improved the odds of a faster re-opening and economic recovery. Small caps as well as cyclical stocks have outperformed the market over the past six months. However, most intermarket relationships are indicating that this outperformance is in its late innings and investor should look to reposition portfolios. Here is a look at the Dark Arts of Intermarket Analysis. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  GameStop’s (GME) Lightning in a Bottle

Everyone loves an underdog story and boy do we have a great one. Make no mistake - DAVID (LINK) - found an inefficiency. He found a boat that was tilted too much on one side (too many funds betting on lower prices) – and flipped it over. He beat Goliath (Wall-St’s elite) at his own game. Markets are a meritocracy. The best ideas always win, regardless of who or where they come from. However, a group of retail investors by themselves - CANNOT ever change market dynamics for too long. Not even in single securities. Other sophisticated funds took full advantage of the market dynamics. Then the unexpected happened. A good investment thesis then escalated into an anti-establishment movement. A movement that is looking for justice for Main street – one that is expressing the frustration felt by masses that feel disillusioned - and feel left behind. The score card, GME rose 400% in a week, a one-in-a-hundred-year event. Cornering the market Several stocks shot up like rockets last week. These are markets that are cornered by artificial constraints, not by fundamental changes in businesses. However, nothing is ever new in financial markets - simply because human behavior never changes. While the narrative is always different, the iteration of fear and greed is always the same. Speculators have been cornering markets since the beginning of time – from railroads, onions, silver, and now ….. in various securities. (LINK). It is purely an artificial scarcity in supply – which works for a short period – but always ends badly for the speculators. The Un-intelligent Investor Media outlets have reported a change of the guard. After a decade of mostly investing in index funds, the retail investor is engaged. In the case of GME and other stocks this week, a small percentage of early investors will reap handsome rewards. The majority will lose … and lose big. Stocks over time go to what the business is worth. There are no exceptions. Does anyone really believe that GME, a brick-and-mortar videogame middleman, is worth a $100/share, let alone $300/share or $22 Billion in equity value? In the worst case, regulators will step in, to stop a run on the markets. Losses will only bring more disillusionment, further emphasizing that the system is rigged against the little guy. It is sad. Markets offer unlimited opportunity to those who are willing to get rich slowly – and unlimited losses to those looking to get rich overnight. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. A new year brings a flurry of investment predictions. While putting precise targets on where markets end the year is silly, working through a list of big picture pros and cons is a good intellectual exercise. Markets are forward-looking, and this exercise helps un-anchor from the events of the past and take an inventory of the future. Here is a list of a few things that I consider important. Here are the Pros.

Always bet on human ingenuity. The list of potential setbacks is long: 1) The vaccines might not be as effective as advertised, 2) new strains might accelerate the spread of Covid, or 3) a large portion of the population might not take the vaccine. However, I believe the likely case is that vaccine logistics and treatment availability will improve, and most at-risk populations will receive a vaccine. This points to a higher probability of ‘life back to normal’ in 2H 2021. Strength begets strength. Public companies survived due to their scale while small businesses took the brunt of Covid. As we return to normal, the scale benefits will magnify the competitive advantages of larger enterprises. This is an underappreciated element of the market advance. Durable operating leverage. Businesses were forced to rapidly cut costs during Covid. Revenues will grow faster than expenses as the economy returns. Earnings growth will remain strong and profit surprises will continue for multiple quarters. Improved household finances. It has taken more than a decade for consumers to recover after the near-death experience of the financial crisis. A combination of forced savings of ‘everything from home’ in 2020 and help from government stimulus has left consumer finances in a strong position. Strong new business formation. The latter half of 2020 had the highest new business formation in over 15 years. Large cloud platforms, social networks, and global marketplaces have created a plug and play system for new business owners. Entrepreneurs can focus on their core skill set and outsource the rest. Here is a list of Cons… Peak QE. The Fed is growing the money supply by 25% annually. It is unlikely that this rate of money pumping will be surpassed and therefore serve as a headwind to market multiples. Interest rates are too low. The justification for above-average valuation is based on historically low-interest rates. If rates stay this low over the next 5 years, stocks will go a lot higher. However, a rebounding economy and economic stimulus will force interest rates upwards. While this is a normal course for a typical economic cycle, this cycle is quite atypical. A rapid rise in interest rates will be turbulent for markets. Valuation above average. While current market valuation is above average, it has to be viewed in the context of ultra-low interest rates and a once in a 100-year pandemic. Most businesses will get back to a normalized earnings trajectory in 2022-23. Understanding valuation within that context makes it a mild negative. Return of the individual investor. The rise of the Robinhood trader has brought on a new level of option speculation. The size of YOLO (you only live once) speculation has grown and this lottery call option buying is the biggest near-term risk to the market. However, this is a microbubble that will dissipate over time without causing a major market event. In hindsight, 2010 or 2017 was a great time to invest, but felt uncomfortable, or at times …. wrong. 2021 is no different. As investors, it is paramount to look at opportunities and risks dispassionately. Valuation is a deterrent to returns at extremes, and we are far from that. We are emerging from a deep recession, with a long runway for economic and earnings growth. Markets have partly anticipated that and are likely to enter a period of consolidation (choppy sideways move). In the big picture, the pros outweigh the cons by a large margin and we are still in the early innings of a multi-year market cycle. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. For the Eye care community, the year ’20-20’ was supposed to be the year of Perfect Vision. It turned out to be anything but that. The world was chaotic. While the markets reflected our societal chaos for some time, they rebounded with a fury that very few believed in. Central banks and governments globally responded by pumping money into markets and with a speed that we had never seen before. When it became clear by the middle of 2020 that a vaccine would be ready within 6-9 months, it was clear that an economic expansion was inevitable. Remember that markets are forward-looking mechanisms, and if the Pandemic of 1918 ran its course in two years, why would Covid-19 last much longer than that? While the market’s reaction has surprised some, it is rational and logical.

I wrote about the most important and profitable investment themes of 2020 ..... well in advance!

The question that I get most is – will the market crash in 2021? The simple answer to that is ‘I have no idea’. I hope that my inter-market process that picked up on the Covid crash will come to my aid again and help in avoiding another meltdown. In all honesty, that is the wrong question. We are in the early innings of a (2-3 year) economic expansion and all my energy is focused on multiple emerging themes that I am chewing over and excited to write about. A simple heuristic is …. watch the Fed. When the Fed over-tightens - and the Fed will - markets will peak, and the next economic downturn will ensue. Every recession has started with an overtightening, and the next one will not be an exception. Until then, focus on the opportunities at hand. These notes serve as a real-time diary of my investment operation. I hope it has helped bring clarity to your thinking. I am grateful for the feedback that I have received. I look forward to those. I say this begrudgingly – knowing that many are hurting – Latticework had an incredible year in 2020 and I look forward to writing more consistently in 2021. While 2020 was far from the year of ‘perfect vision’, I pray that 2021 does not disappoint the Eye care community once again. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. If you missed Part I, here is the link (Part I)

The restaurant business has extremely low barriers to entry. Although the failure rate for restaurants is high, new ones open all the time. This revolving door of restaurants is great for variety, not for building loyalty. Margins in this business are structurally low, to begin with. The pressure to discount and to spend more on sales and marketing costs eats away at any remaining profitability. With this backdrop, even a minor hit to sales pushes this business to be unprofitable. COVID is a crushing blow to the sole restaurant entrepreneur – one who was long on grit - and short on resources. It is virtually impossible to sustain a small restaurant business, operating only at 70% capacity for an extended period (here is why). Therefore, the National Restaurant Association expects tens of thousands of small restaurant operators to permanently close their doors. Large chains can tap into multiple resources that small operators lack. They have bank borrowing lines, the ability to raise alternative capital, and the scale to negotiate with landlords for rent relief or deferral. These chains have invested in the right partitioning of the dining room for safety, built patios to enlarge seating space, and focused on building own delivery channels to complement the aggregators. Chains are share gainers again. A crisis also provides the urgency to streamline. Smaller menus, tighter operating procedures, and removal of all non-essential costs amount to real savings. These chains are already reporting surprisingly high margins for the low level of sales. Most of these eliminated costs will take a long time to creep back. The experience after the Great Recession clearly demonstrated this. The large chains with deep pockets have significant scale advantages, and they are flexing their muscle to their full capacity. Let us step back for a minute and think about supply and demand curves, or Economics 101. When supply in a certain market is overbuilt, two things must take place to reach market equilibrium: 1) a rise in demand, or 2) an exit of supply. Generally, both happen slowly, and over time. However, the case today is not in any Economics textbook. They supply of restaurants will exit the market as the pandemic continues. Demand for eating out dropped 90% in the initial weeks of the pandemic, has improved in the subsequent months, and is now running at negative 40%. At this rate, it is still incredibly difficult for most small chains to continue operating, bringing more attrition. At some point in the future, a vaccine or a health care solution will come to the market. We all intuitively understand the pent-up demand for the forbidden fruit! Who does not want to go out with friends and relax over a meal? Demand for dining out will snap back – overnight! Restaurants that have survived, will boom. The chains will eat most of this share. These restaurant chains will earn higher revenues at higher margins. However, the supply of restaurants will return much slower. Therefore, revenue and profit growth will sustain at a higher level, for much longer than most are willing to believe. The Dine-out industry will bloom again. The survivors will reap the benefits. The Chains will be massive winners. Markets are short term oriented and do not believe this outcome. There will indeed be lots of ups and downs. However, thinking long term is the only path to success in investing. Over time, the forbidden fruit will have juicy returns. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. Over the past three decades, restaurant businesses have been the beneficiaries of multiple secular tailwinds. In the ’80s and 90’s, the suburbanization of America, and a large number of women entering the workforce created strong tailwinds for restaurants. Dual working households, higher discretionary incomes, long commutes, and less time at home; made eating out an easy option.

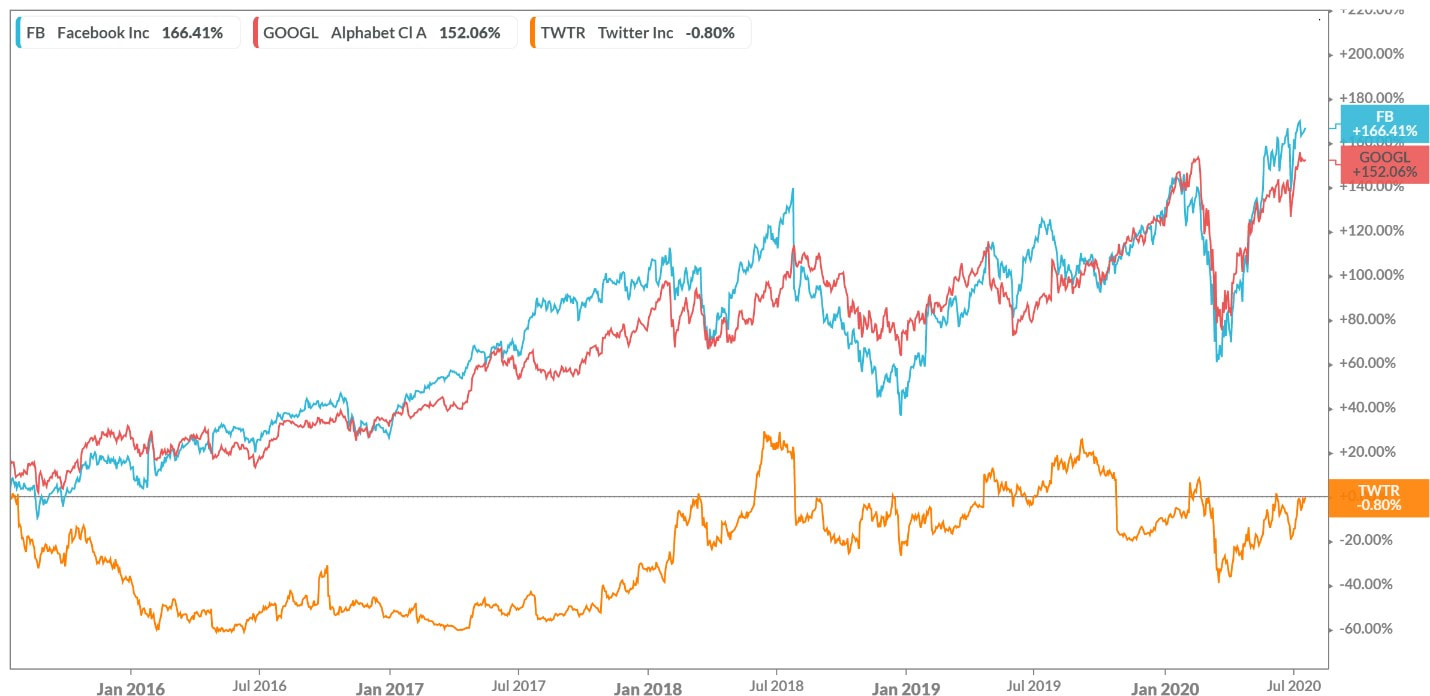

Restaurant businesses who already possessed strong unit economics (What are Unit Economics?) – capitalized on these strong societal trends and aggressively expanded throughout suburbia. As these businesses grew, the scale benefits entrenched multiple moats. They hired the brightest real-estate minds. Access to capital and in-house expertise bought access to the best new locations. Growing sales meant they could afford to spend more on advertising and buy mind share. Scale also brought along purchasing efficiencies for food and commodities. Profitable restaurants also attracted the best managers and provided a deep talent pool to sustain growth. These were powerful tailwinds that most mom and pop restaurateurs could not compete with. Over a quarter century, mass casual dining won a large share of eating out dollars. The successful chain businesses grew from a handful of units into the thousands over multiple decades. Moats are powerful and they last longer than most investors think. But eventually, even the strongest disruptors get disrupted. Overtime, these chains had to slow expansion as they ran out of the best locations. The decade of mobile phones and e-delivery turned us into immobile couch potatoes – which reversed the secular trends for casual dining restaurants. This way of life invited the delivery aggregators to the dining table. Mom and pop operators were faster to embrace the delivery aggregators which provided a growing mind share and an even playing field. Population trends also reversed towards urban living for the past decade. The casual dining chains that dominated for two decades, aged, and slowly lost relevance and connection with their customer. Over the past decade, the mom & pops have won back some of the share they lost over the previous two decades. Until COVID. Part II Next week. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  A few months ago, I wrote a post on Value Creation Vs. Value Capture. Here are additional thoughts, on the dark horse of social media. Twitter.

Google connects seekers of information to relevant content. Facebook connects our personal network. Both companies have leveraged the value they create for users and built great business models. Therefore, both Facebook and Google capture a lot of value for themselves and their investors. On the surface, Twitter is a social network. However, once you use Twitter, one realizes that the core use case of Twitter is vastly different. It is an interest network or a hobby network. I use Twitter for one major reason -Investments. I connect with other investors, network, share, and discover relevant content. You can connect with me @LatticeworkInv. Over the years, Twitter has become indispensable to my investing process. Twitter also offers incredible value for discovery, connection, and curation to users in other interest groups. Sports, Science, Politics are just a few. Despite this value creation for users, the business of Twitter has been unable to capture any of this value for itself and its investors. Over the past 5 years, Facebook's’ business value has increased by 164%, Google’s value has increased by 152%, while Twitter’s value has decreased by 1%. Why? Has Twitter effectively communicated the value that its network offers? To most non-users, Twitter is either for celebrities or interesting people. “I don’t have anything to say” is the most common gripe of non-Twitter users. The onboarding process is un-intuitive. Therefore, even when someone tries to use the product, it discourages them. Despite a similar duration of existence, Facebook has 180 million users in the U.S., Twitter only has 33 million. Most importantly, Twitter lacks a targeting algorithm for advertisers to effectively reach relevant users. For example, most of the Ads that I see in my stream have low relevance to me. Therefore, an advertiser’s return on investment on Twitter is much lower than competitors. Fewer users, fewer advertisers equal fewer revenues and profits. The past only equals the future if you live in the past! Twitter has opportunities that it can capitalize on with the right improvements. Only time will tell. In the rise of personal computing era in the 80’s and 90’s, Microsoft and Intel captured the majority of the value, while the hardware manufacturers fought over the crumbs. In mobile internet era, Facebook and Google have captured the majority of advertising dollars. Twitters creates value, but cannot capture it. The efficacy of the business model makes all the difference. Entrepreneurs focus on building value for customers. Value creation is important, but not enough. Building a business model that can capture that value is even more important. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. The narrative this week suggests that Chinese markets are rallying because the Chinese Govt. is encouraging citizens to buy stocks? Is it that simple? Are global institutional investors wading into Chinese markets on the recommendation of the Government? Chinese markets are rallying for the following reasons - 1) Dollar stalling 2) Improving fundamentals 3) Reasonable valuation 4) Covid under control Can emerging markets finally outperform after a decade in the shadow of the S&P - led by China? Check for yourself. ---

This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. |