The U.S. consumer has been the “Unstoppable Force” for several decades. Despite constant prognostications of his or her demise, the U.S. consumer has shown the willingness to power through every setback. He has fought high inflation, catastrophic job losses, civil unrest, and the great recession. This unique engine of growth - the spine of our economic framework - is 70% of the economy and a centerpiece of global growth.

While there was a laundry list of reasons for his demise, a pandemic is a worst-case scenario. In a service dominated economy like ours, the shutdown of small business – which is high on GRIT but low on financial resources –– severely cripples the consumer. The two pillars to our economy are 1) employment, and 2) lending. A loss of millions of jobs shuts down spending, which leads to more job losses. When the consumer shuts down, so do lenders. Why would any private entity offer a loan when the probability of payback is greatly reduced? The lack of jobs and void of lending creates a negative feedback loop that becomes hard to break. The true solution – a vaccine – is many months away. The unstoppable force is now in a downward spiral at breath-taking speed. The Federal Reserve is the “Immovable Object.” Within its arsenal is the power to create unlimited money. In their words ‘there is no limit’ to what they can do. The Fed has stepped in before to solve crises and has been rightly or wrongly criticized for its actions. Generally, it has moved very slowly, and acted when forced to act. Realizing the gravity of today’s situation, the Fed has moved at lightning speed with incredible force. As traditional lending steps away to minimize losses, the Fed has pledged to back every business, and do whatever it takes. As usual, there are a lot of critics, but letting businesses fail accelerates our downward trajectory and creates more rubble on Main Street. While the Fed cannot create jobs, or generate demand, they can lend to keep the wheels greased. As citizens and consumers, we hope the Fed can buy enough time for researchers to work a miracle cure or at least a viable treatment. But as investors, we are in unchartered territory. There are no Playbooks. While every expert has a loud opinion, the best move today is to stay optimistic - to learn a lot - and do very little. More likely, great ‘one-off’ opportunities lie in the future. The unstoppable force is meeting the immovable object. We hope the good guys win. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.

2 Comments

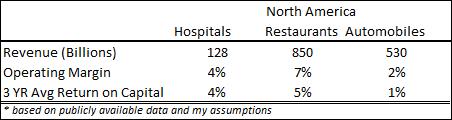

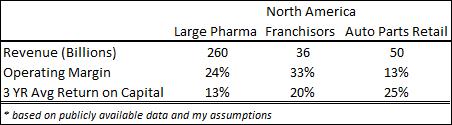

Since times of maximum chaos are fertile ground for opportunity, it's worthwhile to revisit the building blocks of business value creation. Let’s start at the basics. A business creates a solution to an existing need and sells this solution in the form of a product or service. The profitability of this business depends on 1) the value it creates for its customers, and 2) a piece of the value this business can capture and keep for itself. We can measure the success of this value capture on two simple metrics: 1) Operating margin, and 2) Return on Capital. We generally assume that if the potential market size is large, the profit pool will be just as large. However, this is profoundly untrue. In no way is the size of the profit pool related to the size of value creation. Once we examine these three groups: 1) Hospitals, 2) Restaurants, and 3) Automobiles; it becomes immediately clear that despite the large benefits of health, social connection, and mobility to a very large population, businesses within these groups haven’t been able to capture the value they created for customers.  But if we take a step back and examine various groups of businesses within the entire industry, things get clearer. In aggregate, this value chain - a cumulative result of a series of activities of multiple participants - creates a certain amount of total value. And generally, a select few groups within the chain fare substantially better than the overall group. Why is this the case? Well, it has to do with competition, regulation, and capital consumption. The most important component of investing is to understand 1) the total value created by the value chain, and 2) to identify the key cogs in this wheel. Not all participants are entitled to equal profits. Let’s look at the three groups below, who belong to the same industry as the example above:  The medical industry exists to solve the problem of a patient. While the endpoint is between a caregiver and a care receiver, the entire value chain consists of insurers, equipment companies, contract R&D companies, pharma, hospitals, physician groups, etc. If you are part of this industry or have studied it, you might already know who captures the majority of the profits here. Pharma companies and insurers have always been much better investments than hospitals or physician groups.

Similarly, the restaurant industry in the United States is a large and fragmented industry. We like to dine out frequently to whet our appetite for variety and build social connections. But the restaurant business is highly competitive with no barriers to entry, high human capital turnover, and high failure rates. Despite the competition, Franchisors are highly predictable and profitable. The Franchisor model combines the best of both worlds: the entrepreneurial spirit of the franchisee with disciplined, systematic thinking of large corporations (product development and marketing). Therefore, long term financial results of franchisors are very attractive in a poor industry. The automotive business is no different. Despite providing a real utility to drivers and passengers - imagine a world without cars - the automotive manufacturing business is highly competitive and lacks differentiation. And over many decades, its proven to be a bad business. But within the auto value chain, auto part retailers are very profitable. Their competitive advantage is a distribution system that creates a high availability of parts for customers. And the results speak for themselves in the form of high margins and return on capital. Next time, you think a certain product or service would make a good investment, stop and think twice. Ask yourself - What does the industry value chain look like and will this product or service despite its merits, capture part of the value for itself that it creates for customers? --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. For the past several years, OPEC producers have continued to cut their own production in order to maintain reasonable Oil prices. OPEC countries depend on this revenue to balance their own fiscal budgets. However, this price stability gave a green light to U.S. Shale producers to grow their own production – which in turn forced OPEC to reduce production even more. This was an unsustainable situation but was manageable as long as global economies were growing.

Covid-19 brought the entire world to its knees and created a massive demand shock for the oil market. The magnitude of the shock and the resulting excess oil supply meant market forces would dictate prices. At the same time, the disagreement among members themselves came to a bubble. To continue the strategy of reducing market share via production cuts while letting Shale-players enjoy the upside became untenable. There was only one way out of this dilemma. The Saudis finally decided to play long-ball. The only long-term solution to let the market balance would be for U.S. Shale-players to cut their supply. They (we) are swing producers after all. The only way to do that would be for prices to stay low for an extended period of time. By raising its production at a time of global demand shock, the Saudi’s accomplished that. The energy ‘Bear Market’ that started in the summer of 2014 is now in its final innings. These are also likely to be the most painful of innings. The Saudi’s rescued the U.S. shale industry by balancing the market in 2016. This time we are on our own. In 2016, there was an overwhelming amount of private capital waiting to scoop up bargains. Four years later, there is no one. Equity investors, private equity investors, as well as bond investors, are all running scared. There is a good reason for investors to turn their backs on the energy sector. Most businesses did not generate an acceptable return on invested capital over this cycle. They threw good money after bad deals and aggressive investment plans. If they didn’t make money in boom times, what are their chances during the bust? Now only the fittest will survive. There are two ways out 1) Either the Saudi’s blink (stop over-producing) or 2) we endure a wave of painful bankruptcies and restructurings. While the former will only provide temporary relief, the latter will bring a lot of pain to all, and a lot of gain to the ones who survive. We have reached the Bottom of the Barrel. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. Over the past month, market participants have been preparing for an eventual correction. Like an iceberg, the majority of this movement happens underneath the surface. However, markets always leave clues and by using the dark arts of Inter-market analysis, one can get ahead of these market moves by analyzing different asset classes and sectors. In this video, I present the evidence as to why its prudent to be err on the side of caution. This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment.

This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  Renaissance Technologies, founded by Jim Simons, has the best track record of growing investor capital. Better than Warren Buffett. Better than George Soros. The Book “The Man Who Solved The Market: How Jim Simons Launched The Quant Revolution” goes behind the scenes to explore the personal journey of Jim Simons as well as the inner workings of Renaissance. If you want to unpack the success of a Code breaker, Mathematician, Pioneer in Quantitative Investing, and now a Philanthropist – this book is a must-read.

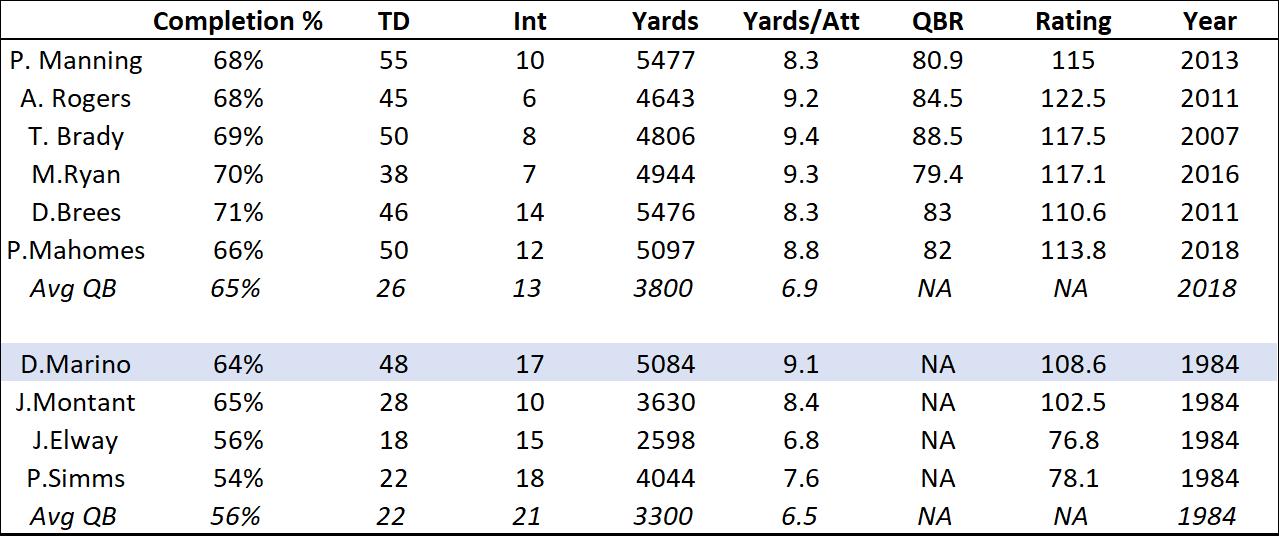

Here are five lessons that I took from the book: 1) Stay Thirsty, my friends. Jim Simons is the real life "most interesting man in the world". He graduated from the best institutions in the world. He worked as a code breaker, built a great Math department at Stony Brook, and then he went on to build the best investment record. Regardless of his success, he always took risks and aspired to reach greater heights. 2) Stay Persistent. He failed for 15 years as an investor, before tasting his first success in the early 90’s. Very few can even imagine the self-belief and persistence it takes to keep going through 15 years of failure. Somehow, Jim found the internal fortitude to keep going. 3) Decentralized decision-making. Jim hired the smartest people and gave them the reins. Many say it, very few do it. This culture of empowerment created a great team that wanted to push the boundaries of success. He also rewarded employees generously and made them part of the team's success. 4) Open Culture. The ‘programming code’ is Renaissance's secret sauce, and it would have been easy to keep it under maximum security. But everyone had access to it - even the secretaries. Any employee could try to improve the code. This level of openness and empowerment did wonders for team morale. 5) Humility. Jim Simons was always approachable and led with humility. During tough market times, he did the unthinkable in the Quant world of overriding the programs knowing well that ‘algorithms can fail’. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  A generational talent in the NFL is one that has all the physical attributes to succeed at the highest level, along with the intangibles such as leadership, IQ, Poise. If we had a dollar for every time we’ve heard this…. Whatever the ‘IT’ factor is, Andrew Luck, as far back as we have followed him, had ‘IT’ and more. At Stanford, he was compared to Peyton Manning, and rightfully so. Despite lack of coaching talent and continuity, no one was surprised that he succeeded in the NFL, and succeeded right away. Luck has the record of ‘Most winning drives by a rookie QB’ in the NFL1. He also went to three straight Pro Bowls in his first three seasons. We all remember watching the playoff performances, and the come-from-behind wins, thinking, “This guy is the real deal”. Injuries made him a bit of an after-thought for two years, but he had a strong comeback year in 2018. And then, ‘Luck’ ran out and retired. You know the story. Most students of history know that a ‘sure thing’ doesn’t exist. This is especially true in the NFL. But does that ever stop us from proclaiming the next great player? No. While he is last on the Montana/Elway/Marino triumvirate, I am quite sure that in 1984-85, Dan Marino was ‘Next’. That year, at least in my books, Dan Marino had the greatest QB season of all times. See the list below. While the top 6 are great players performing at the pinnacle of their profession, these records were made in modern times. But things were different a quarter-century ago! Defensive players could play. What is truly staggering, is the wide margin between what Marino accomplished vs. the average performance in the mid-’80s. Pre 1984, the single-season touchdown record was 34. He shattered most records with ease.  The top panel has the 6 best QB seasons, in no order. The bottom panel contains the stats from 1984

But after the epic sophomore NFL year and a Superbowl appearance, Dan Marino never quite attained the same heights. Whether it was coaching, injuries, overall team talent, or preparation and desire; the exact breakdown we shall never know. But the proclamations of multiple Super Bowls wins turned out to be false. His peers - Montana, Elway, Simms, Kelly - went on to play and win the Super Bowls. Which brings me to the most recent sensation – Patrick Mahomes. Mahomes had an incredible season for any QB, but more so for a first-year QB. He is a ‘generational’ talent, and therefore, Mahomes is now ‘Next’. But we know better, don’t we? Money, fame, injuries, arrogance, team and coaching turnover will constantly push him off this pedestal. The ultimate lesson and reminder in all of this is of our mediocre ability to forecast the future. We, along with the world are constantly changing, in ways, we don’t fully understand, and our tendencies to pattern-match people, situations, and businesses by putting them in certain boxes or using heuristics, isn’t enough. Excel couldn’t do it the past, and I doubt A.I. will come close in the future. --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. The case for curbing the power of Facebook, Amazon, Google, and Apple (FANG) is well documented. The scale and scope of these businesses is virtually unprecedented, and therefore it was a matter of time that the Anti-Trust authorities went after them. Here is the short version of the Anti-Trust case: Amazon is unfair to sellers on its marketplace, Google shows preferential treatment to its own properties, while Facebook uses a dominant social media position to utilize user data in harmful ways that we don’t fully understand.

Anti-trust laws were developed over the 20th century to ensure fair competition to protect customers from predatory business practices. Therefore, the real question that should be asked is: are these businesses unfair to customers? Let’s revisit the breakup of the AT&T business. AT&T in the 1970’s controlled every aspect of communications. It made the equipment, was miles ahead on R&D, and owned and operated the infrastructure for all local and majority of long-distance service. AT&T had aggregated the supply of telephone service into a powerful monopoly which discouraged competition and gave customers no choice. Well, one choice - AT&T. Therefore, AT&T had to be broken up into multiple companies to introduce competition and better prices/services for consumers. Let’s consider another example – the local monopolies of cable companies. For several decades, when one moved into a condo building, the list of options for cable and internet was already narrowed to 1. It was based on who had wired the building. Neither you nor I had much of a choice. The cable company had aggregated the supply of entertainment (cable channels etc.) and gave the consumer no choice but the small list of packages. This situation goes unaddressed. This aggregation of supply of product and services into the hands of a few providers is clearly bad for competition and for consumers. In my opinion, the case against today’s giants doesn’t hold water. The business models are different, and products are superior. As a result, most consumers love these businesses and spend a lot of time using them. As Ben Thomson at Stratechery has written this ad-nauseam in his ‘Aggregation Theory’, the core difference between FANG and the dominant businesses of the past is who/how they are going about aggregation. In the past, the strong businesses consolidated the supply of products and services, became the sole offering, and therefore left consumers very little choice. Today, FANG has built products that have provided tremendous value and convenience to customers. In some cases, they are cheaper than the alternative. And therefore, rightfully so, they have won total consumer loyalty. Loyal customers are the real reason FANG enjoys dominant market power. They have consolidated demand – the consumer – and therefore left no choice for suppliers but to deal with FANG. As an end result, FANG is exerting its market power on its suppliers for the benefit of the consumer. I do not have a legal background nor do I have any insight into how these proceedings will eventually work out. It could very well be that these businesses use their unprecedented power to abuse consumers. But can we punish someone based on a crime that haven’t committed? No. Until that changes, the anti-trust case against FANG is weak at best. What do you think? --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future. When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact - Warren Buffett

Can Tesla save itself from Elon? “Wait a minute! Elon built Tesla” is usually the first response. Yes, but when the builder starts burning down the house, the house must be saved from its builder. The story of Tesla has parallels to Apple- not today’s Apple, but the Apple Computers from the ’90s. Apple’s core customers were die-hard fanatics - but the business model was flawed - therefore it experienced multiple near-death moments. Similarly, Tesla has products that are loved by customers, but the business architecture is flawed. And who else can we blame that on if not the chief architect itself, Elon Musk. Let’s start at the very beginning. Instead of confining the Tesla business as a high-end, niche car manufacturer – ala Ferrari - Elon went the route of a mass market company. The mission of the Company is to ‘accelerate the world’s transition to sustainable energy’. While the mission is admirable, businesses need sound economics to be successful. This was a grave mistake as the capital demands and fixed costs for a mass market operation are in the stratosphere. It’s a long climb to gain scale, and with the slightest slip-up, you slide down to the bottom of the pit. In the past, the generosity of capital markets made up for the slip-ups, but as we all know, Mr. Market has a fickle disposition. Tesla had a great start with the Models S and X. It should have stopped there. Elon made a splash by announcing the Model 3, without ever knowing if he could deliver on his promise. He bet the future of Tesla on his engineering prowess and on the concept of a fully automated factory floor that could churn out cars at a much higher rate than humans could. The lower operating costs would make the $35,000 price tag work. However, there was no proof of concept. This was another fatal mistake. The result is a Model 3 where the Company loses money on every sale. While this is a great ‘social’ scheme, what is the business rationale for selling more Model 3’s? Every incremental sale accelerates Tesla’s demise. But let me explain how it gets worse. The price tag is too high which makes it unaffordable for the masses. The high-end version Model 3 is cannibalizing the sales of Model S – which is a profitable car. It has also led to a slowdown in the sales of Model X. The cash crunch led Elon to unwind its retail store operation. It will be very difficult to convince a mass market customer to purchase a car online without first test driving a vehicle. The early adopters already own Tesla cars. How do you grow the business? The long list of executive departures over the past 18 months has been a warning sign. But it is also a symptom that the culture of Tesla is rotten at its core. The multiple employee lawsuits also point the finger in the same direction. While a great inventor, Elon is a poor manager. Ultimately, the accountability of a poor company culture rests with the CEO. Elon Musk has also been adamant that Tesla doesn’t need to raise capital. 4Q18 presented a great opportunity for the Company to raise capital at attractive terms. But believing his own rosy forecasts, Elon passed. This was another colossal failure on Elon’s part. Finally, as the Company is almost running out of cash, Tesla raised $2.8 billion in May 2019. It’s almost too little and too late. At this rate, the Company will need another capital raise by year end. The terms will get more and more onerous. While most of the equity valuation might not be salvageable, the brand and most of the 40,000 jobs that are on the line can still be saved. What is in high order is for the absentee Board of Directors to step in and act as fiduciaries. The Board needs to act in keeping the long-term interests of the business and employees in mind, not Elon’s fantasies. That requires rationalizing the business by focusing on the profit centers. The purpose of this business, like any other, is to generate economic value, not unprofitable sales. A sustainable business is good for society, not a walking zombie-like Tesla. I addressed the core issues of demand, employee turnover, lack of capital in Trouble under the Tesla hood last August. These chickens have come to roost. Now, it’s time for the Board to save Tesla from Elon and salvage whatever it can before it’s too late. -- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  T’is the season. IPO season. The winds are behind the market’s back and the window to parade out shiny new IPO’s is open. After all, investors get tired of talking about the same, boring companies. We all crave sizzle. So, the Bankers have arranged for a great parade. A 'Parade of Unicorns' such as Lyft, Zoom, Pinterest, Slack, and the biggest unicorn – UBER.

So what IPO are you buying? This is a question I get often. And I have a boring answer. None. It's not that I am not interested in shiny new objects. I get enamored by fast-moving-rocket ships just like the rest. But I have investment rules - and staying away from IPOs - is one of those rules. As usual, a small number of IPO’s today will be the great companies of the next decade. If you have that unique insight, you should jump aboard. But it is difficult because we don’t have enough information. It’s no different than picking players in an NFL or NBA draft. The majority won’t pan out. Here are three reasons to stay away from IPO’s. 1. An IPO is a Cinderella tale. The Banker ‘s involved in selling the deal, first take stock of the prevailing investment narrative. Then they hatch a plan with management to show the ‘story’ in company financials. For example, if investors are thirsty for growth at all costs, the company goes for broke a year prior to IPO. If investors are campaigning for spending discipline, then the Company pursues margin improvement. Get it? However, in most cases post IPO - when the clock strikes midnight and business conditions sour- the business model, and cash flow turns into pumpkin and mice. Believe me, I have IPO scars to prove it. 2. An IPO represents the uber-smart, insider, early investor who is selling. Bill Gurley, at Benchmark, a great Technology investor, will be a seller in the UBER IPO. Do I want to be the buyer on the other end? No. What asymmetric information advantage do we have over Bill Gurley? None. 3. But most importantly, acting on an IPO is acting on sellers’ terms. As investors, we want to act when the time is right for buyers to buy, not when its right for sellers to sell. It is easy to say and very hard to do. And therefore, as investors, we need a rules-based process. According to poker player and author of ‘Thinking in Bets’ Annie Duke, it is much easier to decide and stick to ‘I won’t eat any carbs’ vs. ‘I will try to limit carb intake’. The former is one, firm, commitment vs. the latter is a meal-by-meal judgment. The former is much easier to execute. The reason most diets fail is that most of us do the latter. I am staying away from the oncoming IPO frenzy because it is part of my rules-based process. Before you decide to invest in an IPO, ask yourself one question. Why do you want to take on Bill Gurley? --- This material does not constitute an offer or solicitation to purchase an interest in Latticework Partners, LP (the "Fund"). Such an offer will only be made by means of a confidential offering memorandum and only in those jurisdictions where permitted by law. An investment in the Fund is speculative and is subject to a risk of loss, including a risk of loss of principal. There is no secondary market for interests in the Fund and none is expected to develop. No assurance can be given that the Fund will achieve its objective or that an investor will receive a return of all or part of its investment. This material contains certain forward-looking statements and projections regarding the future performance and asset allocation of the Fund. These projections are included for illustrative purposes only, are inherently speculative as they relate to future events, and may not be realized as described. These forward-looking statements will not be updated in future.  The month of March marks 500 years since the passing away of Leonardo Da Vinci. Several museums around the world have set up exhibitions to celebrate Leonardo’s legacy. Inquisitive minds would like to know: 1) How brilliant are the accomplishments for one to be celebrated after five centuries? and 2) If ‘genius leaves clues’ what can we learn from the extraordinary ‘ones.

While I spent several hours reading broadly in admiration of Leonardo, the book “Leonardo Da Vinci” by Walter Isaacson is by far the most concise work on his life. The Last Supper and the Mona Lisa are two of Leonardo’s seminal works, but the totality and the range of his accomplishments is well beyond the popularity of these paintings. Leonardo was also the first to accomplish many things. Outside of painting and sculpting, he was interested in architecture, engineering, human anatomy, physics, and optics. He was the first to create a modern-day map and to discover that the human heart had 4 chambers, instead of two. He intuitively understood that the study of optics is important to bring the right perspective to the viewer. He left behind 7000 pages of notes, where he wrote: “Painting is based on perspective, and perspective is nothing else than a thorough knowledge of the function of the eye.” His greatest accomplishment though was the intense focus and curiosity with which he approached the ‘mundane’. When the World saw a bird, he zeroed in on the ‘mechanics of the tongue’ – which differentiated his insights. He dissected the human body to understand human anatomy. It is unthinkable even today for an artist to do that. He was a missionary in the quest of knowledge, instead of a mercenary who produced for money. He devoted his life to mastering the Sciences, the Arts, and Humanities. It is this unique combination that produced his ‘body of work’. The study of Leonardo’s life and achievements brings three conclusions: 1) Broaden our Perspective. Society and educational status-quo preach focus and mastery of narrow topics. However, to create true differentiation and transcendental works, one must combine multiple disciplines. We must broaden our perspectives. A well-understood example is how Apple combined hardware, industrial design, and packaging aesthetics to build a brand in a crowded field. It is not surprising at all to learn that Steve Jobs idolized Leonardo 2) Take Risks.In a world where everyone is focused on instant success and immediate positive feedback, the willingness to take risks with our scare capital (time and money) to purse ideas that might not be popular in the present is a structural advantage. 3) Delayed vs. Instant Gratification.In investment parlance - reading widely outside of finance and business – brings differentiating insights which are not obvious at the time of reading. It’s the ‘eventual connecting the dots’ that makes a big difference because only a select few are going down this road. This is truly why - forgoing immediate investment success - to invest in what is less obvious - results in sustainable and long-lasting returns. |